The conclusion of the 2023/24 tax year prompts us to reflect on some of the notable developments in the fiscal landscape.

This past year has been marked by ongoing efforts to recover from the economic impact of the global pandemic. Inflation has emerged as a significant concern, influenced by persistent disruptions in the supply chain and geopolitical tensions.

To address these economic challenges, the Government has adjusted tax policies to balance revenue generation with support for businesses and individuals.

The regulatory environment has experienced continuous flux, requiring businesses and individuals to be adaptable in order to stay compliant.

The Chancellor of the Exchequer, Jeremy Hunt, presented his 2023 Autumn Statement to Parliament on 22 November 2023, publishing the supporting documents, while the Office for Budget Responsibility (OBR) published updated forecasts for the UK’s economic and fiscal outlook.

The Chancellor said the Autumn Statement set out “growth measures to back British business” and “measures to make work pay”, two themes we expect to see revisited in the Spring Statement.

So, as we conclude the tax year, we look ahead with anticipation for potential future reforms. This highlights the importance of adaptability and resilience in tax planning and navigating the fiscal landscape.

With that in mind, we crafted this year-end tax guide to provide you with insights, enabling you to start the new tax year on solid ground. In this guide, you’ll find succinct summaries of the primary tax reliefs and allowances applicable for the remaining months of 2023/24.

Each section is accompanied by a set of planning points, serving as a practical checklist to help you consider all essential areas.

If you have any questions or want to delve deeper into your tax planning, please reach out to us. We’re here to assist you in navigating the financial year.

Minimising your personal tax bill

The personal allowance is £12,570. Non-dividend income above this threshold is taxed at rates from 20% to 45% (or 19% to 47% in Scotland).

A higher marginal tax rate may be payable between £100,000 and £125,140 as the personal allowance reduces by £1 for every £2 earned above £100,000. This means those with non-savings and savings income in this band have an effective tax rate of 60% (63% in Scotland) for this tax year.

You may be able to transfer £1,260 of your unutilised personal allowance to your spouse or civil partner if certain conditions are met. This is known as marriage allowance and could save couples up to £252 in income tax in the tax year.

Tax on savings and investments

The personal savings allowance allows a basic-rate taxpayer to receive up to £1,000 in savings income tax-free. A higher-rate taxpayer can get up to £500 in savings income without any tax being due. There is no relief for additional-rate taxpayers.

If you earn less than £17,570 annually, you may be able to receive up to £5,000 in interest without paying tax on it. This is known as the starting rate for savings.

The first £1,000 of income from dividends in 2023/24 is tax-free, while income from dividends that exceeds this amount is usually taxed at rates of 8.75%, 33.75% or 39.35%. In 2024/25, this will be halved to £500, so use the most of your allowance while you can.

Key considerations

- Are you and your spouse or civil partner using all of your personal allowance? If not, consider the availability of the marriage allowance.

- Are there opportunities to utilise any unused allowances this tax year?

- Can you reduce your exposure to high marginal tax rates by retaining your full personal allowance? For example, by paying amounts earned above £100,000 into a pension scheme.

- Is it worth considering tax-efficient alternatives to a bonus or salary increase?

- Can you utilise rent-a-room relief which is £7,500 for individuals or £3,750 for co-owners?

Using your ISA allowance

If you are planning to make the most of this year’s £20,000 ISA allowance, you need to use it before 5 April 2024. There’s no rollover from one tax year to the next.

Growth, income and withdrawals are not liable for income or capital gains tax, but the value of an ISA will form part of your estate for inheritance tax purposes.

Under-18s, or those who wish to save on behalf of a minor, can put up to £9,000 into a junior ISA for 2023/24.

As part of your £20,000 ISA allowance, it’s possible to invest up to £4,000 in a lifetime ISA which receives an annual government bonus of up to £1,000 per year.

You must be over 18 but under 40 years old to open a lifetime ISA, which can be used to buy a first home or fund retirement. Further scheme rules and early withdrawal penalties apply.

Existing savers with help-to-buy ISAs can continue to put up to £200 a month towards securing a mortgage to purchase their first home.

Providing the funds are used to buy a first home, the savings will earn interest and qualify for a 25% government bonus of up to £3,000. The purchase price of the property must not exceed £250,000 (or £450,000 in London).

Key considerations

- If you don’t already have an ISA, should you start one this tax year?

- If you have used your ISA allowance, can your spouse or civil partner put any excess savings into their ISA?

- Make sure you have used the £20,000 maximum tax-free ISA allowance before 5 April 2024.

Saving for retirement

Making the most of the annual pensions allowance is a particularly attractive option for higher earners as we approach the end of the tax year.

Personal tax relief applies to pension contributions, although this may be restricted by the annual allowance or net-relevant earnings.

The annual allowance for 2023/24 is £60,000 for those with an adjusted annual income from all sources, including pension contributions, of £260,000 or under a threshold income of £200,000 or less.

An individual’s annual allowance reduces by £1 for every £2 of adjusted income over £260,000 – down to a minimum of £10,000, although this usually applies to those with a total income of £312,000 or more.

Provided you had a pension fund during a previous tax year, it is possible to carry any unused allowances forward, up to a maximum of three years.

Key considerations

- If you’re over 55, consider the potentially serious tax implications of accessing your pension early – and always seek advice before you do this.

- Do you have unused allowances from previous tax years that are due to expire soon?

- Have you reviewed both your and your partner’s pension contributions?

- Can you afford to pay more into your pension?

- Are you aware of the potential inheritance tax benefits of maximising your pension fund?

- Review your letter of instruction to the trustees of your pension fund.

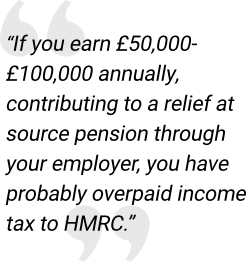

- If you earn £50,000-£100,000 annually, contributing to a relief at source pension through your employer, you have probably overpaid income tax to HMRC. Given the 40% income tax bracket for your salary range, the default 20% relief at source on your pension contributions means you’re missing out on 20% tax relief.

Planning for the future

Inheritance tax is usually charged at a rate of 40% on the portion of your estate that exceeds £325,000.

An extra tax-free threshold of £175,000 – known as the residence nil-rate band (RNRB) – is available in certain conditions. These include if you leave the family home, or a share of the family home, to direct descendants.

The RNRB gives a total potential tax-free threshold of up to £500,000 for individuals – or £1m for married couples or civil partners. However, the band reduces by £1 for every £2 of value by which an estate exceeds the £2m taper threshold. If the estate is left to the surviving spouse or civil partner on the first death, the taper is applied on the second death.

Furthermore, the percentage of any unused threshold allowance or nil-rate band from the first death may be transferred to the surviving spouse or civil partner, allowing up to double the nil-rate band applicable at the date of the second death.

Gifts or transfers made within seven years of death are also added back into the estate and might be taxable.

Taper relief may be available on any inheritance tax due where the gift was made between three years and seven years prior to death.

Key considerations

- Do you have an up-to-date will that reflects your wishes, and are you happy with its executors?

- Are you taking advantage of exemptions, such as the annual £3,000 gift exemption, gifts from income, and gifts on marriage or civil partnership?

- Do you have surplus assets that you can give away and thus potentially reduce the value of your estate chargeable to inheritance tax?

- Should you consider altering the spread of your investment portfolio into more inheritance tax-efficient products?

- Investigate the benefits of putting assets into trusts to reduce the inheritance tax impact.

Stamp duty land tax in England and Northern Ireland

Stamp duty land tax has gone through numerous changes in recent years. During the pandemic, for instance, people who were moving house enjoyed temporary property tax holidays that were in place around the UK.

The stamp duty land tax holiday in England and Northern Ireland was the last to close, ending on 30 September 2021. The pre-pandemic regime returned for the 2022/23 tax year, charging 2% on property purchases above £125,000.

A temporary stamp duty relief was then announced on 23 September 2022 and will remain in place until 31 March 2025, increasing the residential nil-rate tax threshold from £125,000 to £250,000 for residential property purchased between these two dates.

The threshold at which first-time buyers begin to pay stamp duty land tax is £425,000 for property purchases entered into from 23 September 2022, rather than £300,000. Likewise, the maximum value of a property on which first-time buyers’ relief can be claimed is now £625,000, rather than £500,000.

A 5% tax charge applies to the portion of your new property’s value that falls between £250,001 to £925,000. The higher stamp duty land tax rates and thresholds also apply (see table below). For taxpayers trying to purchase additional residential property, a 3% stamp duty land tax surcharge applies where the value is £40,000 or more. This surcharge is added to the other tax rates on the whole purchase price.

| Residential property price* | Rate | Non-residential property price | Rate |

| £0 – £250,000 | 0% | £0 – £150,000 | 0% |

| Over £250,000 – £925,000** | 5% | Over £150,000 – £250,000 | 2% |

| Over £925,000 – £1.5m | 10% | Above £250,000 | 5% |

| Over £1.5m | 12% |

**For residential purchases by ‘non-natural persons’ of more than £500,000, a rate of 15% applies subject to certain exclusions.

Land and buildings transaction tax in Scotland

For people buying a residential property in Scotland, no land and buildings transaction tax will be owed on the first £145,000 of the property price.

The 2% land and buildings transaction tax rate kicks in for homes worth between £145,001 and £250,000.

A 5% rate applies on the slice of the residential property price between £250,001 and £325,000, while a 10% rate kicks in between £325,001 to £750,000. Above this, a 12% rate is levied.

People trying to buy an additional residential property in Scotland pay a surcharge at 6% on properties worth more than £40,000 for transactions entered into on or after 16 December 2022. For transactions entered into before this date, a 4% tax applies. This ‘additional dwelling supplement’ also applies to the total purchase price.

First-time buyers in Scotland pay no land and buildings transaction tax on properties worth less than £175,000. Tax will apply at various rates on any excess above this amount.

Land transaction tax in Wales

In Wales, the pre-pandemic land transaction tax regime has applied since 1 April 2018.

If you do not own other property, no land transaction tax is owed on the first £225,000 of a residential property in Wales.

A 6% rate applies on the portion between £225,001 and £400,000, before a 7.5% rate is liable on the residential property price worth between £400,001 and £750,000.

Above £750,000 and up to £1.5m, a 10% tax rate is in place, and a 12% rate applies to the portion above £1.5m.

You may need to pay higher rates if you buy a residential property in Wales for £225,000 or more and already own one or more residential properties.

Rules, exemptions and allowances

The capital gains tax allowance for the 2023/24 tax year has decreased by more than 50% from its 2022/23 threshold of £12,300 to £6,000. This annual exempt amount is set to halve again to £3,000 in 2024/25.

This means that any individual who makes gains on assets over the value of £6,000 this tax year will be required to pay capital gains tax on the excess amount at their marginal tax rate.

Married couples and civil partners each have a £6,000 exemption, with gains above this usually taxed at a rate depending on their income levels and the type of asset.

Similarly, if you jointly own an asset with another person, you can use both of your allowances to double the exempt amount available (£12,000) before capital gains tax is due.

Where taxable income is less than the UK basic-rate limit of £37,700 (the roof of the basic rate for income tax minus your personal allowance) the capital gains tax rate for most gains up to the remaining basic-rate band is 10%. After this, it rises to 20%, while the standard rate for a trust is 20%.

Gains from the sale of residential properties that are not your main residence are taxed at rates of 18% in the basic-rate band and 28% in the higher or additional-rate bands.

The rate usually applicable to disposals of residential properties by trustees is 28%.

Key considerations

- Have you used your £6,000 annual exemption? This will decrease to £3,000 in 2024/25, so use your tax-free allowance while it’s more generous.

- What can be saved by maximising family member tax-free exemptions?

- To utilise the spouse annual exemption, should you put an asset into your joint names before selling it?

- Do you have other assets that you can used to reduce your gains by creating a capital loss?

- If a negligible value claim can be made on any shares you hold, they do not need to be sold to create a capital loss to offset against any gains made in the tax year.

- If tax is owed, can you defer or rollover the gain, for example by investing the proceeds into a SEIS-eligible investment?

- Have you made a main residence election?

- Did you know that you must report and pay any capital gains tax on the sale of additional UK residential property within 60 days of completion?

- There are a number of reliefs that can help to reduce your capital gains liability, such as business asset disposal relief and principal primary residence relief.

CGT when selling your business

Business asset disposal relief can reduce the rate of capital gains tax due on the disposal of qualifying assets and all or part of your business from 20% to 10%. Prior to 6 April 2020, this relief was known as entrepreneurs’ relief.

To qualify, you must have owned the business for the last two years – either as a sole trader or in a business partnership.

If you sell shares or securities, you may also qualify for the relief if you have been an employee or office holder of a ‘trading’ company for two years up to the date the shares are sold.

You must also have at least 5% of both the shares and voting rights, plus be entitled to at least 5% of either the profits that are available for distribution and the assets on winding up, or the disposal proceeds if the company is sold.

Different rules apply to shares from an enterprise management incentive scheme.

If you are closing your business, the same conditions apply, and you must also dispose of any assets owned by the business within three years. There is no cap on the number of times you can claim the relief, but you can only claim a total of £1m in business asset disposal relief in your lifetime. Prior to 11 March 2020, this lifetime limit was £10m

If you have already claimed business asset disposal relief on gains of £1m or more, any future disposals will not qualify for the relief.

Alternatively, if you have never previously claimed business asset disposal relief, only the first £1m will qualify for the 10% relief, with the rest of the disposal taxable at 20% in 2023/24.

Tax and your resident status

A non-dom is a UK resident whose permanent home, or domicile, is outside of the UK. An individual may have more than one tax residence but can only have one domicile at any given time. Domicile status is incredibly difficult to change and is significant because it determines an individual’s liability to UK income tax, capital gains tax and inheritance tax.

As a non-dom UK resident taxpayer, you can choose to be taxed on either the arising basis or the remittance basis.

Under the arising basis you are taxed as any other UK-domiciled and resident taxpayer would be, on your worldwide income and gains.

Under the remittance basis you are only taxed on your UK earnings and gains. Any income or gains arising outside of the UK are not taxed unless you choose to bring that money into, or enjoy use of it in, the UK. Claiming the remittance basis will cause the individual to lose their personal allowance.

The Government introduced new deemed-domicile rules from 6 April 2017 to limit the time that these beneficial rules can be used.

Non-doms will be deemed UK-domiciled for income tax, capital gains tax and inheritance tax purposes if they’ve been a UK resident for at least 15 out of the past 20 tax years immediately before the start of the current tax year.

If you become deemed domiciled moving forward, you will no longer be able to claim the remittance basis and will be assessed on your worldwide income and gains on the arising basis. You will also potentially be liable to inheritance tax on worldwide assets.

Working-from-home allowance

Employees who are required to work from home may be able to claim tax relief of £6 a week from HMRC. Alternatively, employers can pay the allowance to employees tax-free via payroll.

This cannot be claimed if you choose to work from home – for example, if your employer operates a hybrid working policy.

Electric vehicles

Drivers of electric vehicles and some hybrids provided by an employer pay 2% on this benefit-in-kind.

Hybrid company cars need to be registered from 6 April 2020, have CO² emissions of less than 50g/km, and travel more than 130 miles on a single electric charge to qualify for the existing 2% rate.

The application of other low benefit-in-kind rates will depend on the vehicle’s CO² emissions and the number of miles it can travel on a single charge.

Trivial benefits

Employers can provide trivial benefits worth up to £50 per employee, as long as it’s not cash or a cash voucher, not a performance-related bonus and not included as part of a remuneration package in their contracts. No tax or Class 1A NICs will be due on such items.

Directors of close companies also qualify, although it is limited to six occasions per tax year (e.g. £300 per tax year).

Key considerations

- Have you or your employer claimed homeworking relief in 2023/24? Bear in mind that you might no longer be eligible, even if you previously claimed this relief while Covid-19 restrictions were in place.

- Employers that provide pure electric cars in 2023/24 will save Class 1A NICs and employees may see significant income tax benefits (this may involve a salary sacrifice).

- As part of the benefit. the employer can also pay for vehicle repairs and servicing, car insurance and car tax, and may be able to claim back 50% of the VAT on any lease charges (if VAT-registered).

Understanding the changes

On 1 April 2023, the main rate of corporation tax rose from 19% to 25% for companies with profits over £250,000.

A new ‘small profits rate’ of 19% applies to smaller entities with profits of up to £50,000, while most UK companies with profits between £50,000 and £250,000 can claim marginal relief to reduce their liabilities.

Companies need to keep accounting records and prepare company tax returns.

Payment is usually due 9 months and 1 day after the company’s accounting period, while company tax returns are usually due 12 months after the company’s accounting period.

However, larger companies may be required to pay via quarterly instalments depending on the profits being made.

Business deductions

When you’re working out your business’s taxable profit, you can deduct any costs that were incurred “wholly and exclusively” for the purposes of the trade.

These could include the cost of travel, staff salaries, pension contributions, bills for your business premises, advertising and marketing, and training.

Directors’ bonuses can also be claimed as a deductible cost, as long as they are paid within nine months of the company year-end, and the entitlement to the bonus is established before the accounting date.

You may also be able to claim capital allowances for assets you buy to keep in your business, such as equipment, machinery and business vehicles.

Key considerations

- Think about your company’s expected profits for this financial year. Proactive corporate tax planning can help you minimise the impact of the corporation tax rise.

- If you are due a director’s bonus, have you accrued it in the annual accounts as a deductible cost?

- Have you paid any employer pension contributions? These must be paid before the year-end to get tax relief in the accounting period.

- Are you paying a member of your family a salary? Salaries can be paid to family members as long as they are justifiable and at commercial rates.

- Have you considered tax-efficient ways of extracting profits, such as dividends, pension contributions and benefits-in-kind?

Navigating the VAT system

Around 2.7 million businesses in the UK are registered for VAT, which is usually charged at 20% on the sale of goods and services.

Your business must register for VAT when it has a taxable turnover of more than £85,000 in the previous 12 months or if it expects to exceed this threshold in the next 30 days.

Your VAT taxable turnover is the total of everything sold that is not exempt or outside the scope of VAT. You can voluntarily register for VAT, and also voluntarily deregister if your taxable turnover is expected to be less than £83,000 over the next 12 months.

VAT schemes exist to simplify accounting for VAT, including the cash accounting scheme, annual accounting scheme and the flat-rate scheme.

MTD for VAT

Most VAT-registered firms need to keep digital records of their sales and file monthly or quarterly VAT returns using HMRC-approved software under the Making Tax Digital (MTD) regime.

From 1 January 2023, HMRC moved to a points-based penalties system to encourage good taxpayer behaviour. Stringent rules around the way businesses digitally link their software and upload their VAT returns were also introduced at this time.

MTD for VAT applies to all VAT-registered businesses, regardless of whether their taxable turnover is above the current VAT-registration threshold or not. They are required to use MTD-compatible software to meet their VAT reporting and record-keeping obligations.

Key considerations

- Could your business use one of the simplified accounting schemes?

- Do you need to register your business for VAT?

- Are you entitled to claim VAT bad debt relief?

- Are you accounting for VAT correctly on the fuel used for private motoring? Should you be accounting for the appropriate scale charge?

- Are you reclaiming VAT only where you are entitled to? You are not entitled to reclaim VAT on certain assets or expenses. For example, only certain types of business may reclaim VAT on cars.

- If you are registering for VAT for the first time, you can reclaim the VAT on certain pre-registration expenses including services you have paid for in the six months prior to registration and any goods or fixed assets you still have (or that were used to make other goods you still have) in the four years before registration.

The cost of non-compliance

HMRC issues fines for non-compliance with income tax, corporation tax, VAT and inheritance tax.

The self-assessment deadline for income tax is midnight on 31 January 2024, and you will receive penalties if yours is late. You will also be charged interest on late payments at 7.75% from 22 August 2023.

Late payment interest is set at the Bank of England’s base rate plus 2.5%, so it is subject to change before the end of the tax year.

If you send a late self-assessment income tax return, you will have to pay:

- £100 for being a day late

- £10 a day for a maximum of 90 days for being three months late

- 5% of the tax you owe or £300, whichever is greater, if six months late

- a further 5% of the tax you owe or £300, whichever is greaterv, if 12 months late – in some cases, you may have to pay up to 100% of the tax you owe.

If you delay paying your self-assessment income tax by:

- 30 days – you’ll have to pay 5% of the tax you owe at that date

- 6 months – you’ll have to pay a further penalty of 5% of the tax you owe at that date

- 12 months – you’ll have to pay a further penalty of 5% of the tax you owe at that date.

New businesses also face being fined for not notifying HMRC that they have commenced trading.

If the business is a company then it will also need to ensure it submits its annual accounts ahead of its deadline to avoid incurring a penalty.

Penalties vary from £150 for a private company filing its annual accounts one month late to £7,500 for a public company that files its accounts more than six months late.

IMPORTANT INFORMATION

The way in which tax charges (or tax relief, as appropriate) are applied depends on individual circumstances and may be subject to future change. ISA and pension eligibility depend on individual circumstances.

FCA regulation applies to certain regulated activities, products and services, but does not necessarily apply to all tax-planning activities and services.

This document is solely for information purposes and nothing in it is intended to constitute advice or a recommendation.

While considerable care has been taken to ensure the information contained in this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information.