How to use this guide

As we approach the end of the 2024/25 tax year, it’s a good time to reflect on the year’s financial developments and their impact on tax planning.

The UK economy has continued to navigate a challenging landscape, with high interest rates affecting businesses and individuals alike. Inflation has begun to stabilise, offering some relief, but persistent pressures on household budgets remain. Global economic uncertainty and domestic policy changes have further underscored the importance of strategic financial planning.

The Chancellor’s controversial Autumn Budget in 2024 introduced a mix of measures aimed at balancing fiscal stability with support for economic resilience. While targeted reliefs for small businesses and incentives to encourage investment in key sectors were announced, some changes — such as an increase in employers’ National Insurance contributions — have sparked debate about their broader impact.

These developments highlight the need to stay informed and take a proactive approach to managing your financial affairs.

Tax planning is not just about compliance; it’s an opportunity to optimise your finances and make full use of the reliefs and allowances available before they reset on 6 April 2025. Whether maximising pension contributions, reviewing inheritance tax strategies, or taking advantage of ISAs, acting now can help you minimise liabilities and prepare for the year ahead.

This guide provides a comprehensive overview of the key allowances, tax breaks, and exemptions available, alongside practical planning points to help you take action. We’ve tailored this information to reflect the latest legislative changes, ensuring you’re equipped to make informed decisions before the tax year closes.

If you’d like more tailored advice or help implementing any of the suggestions in this guide, please don’t hesitate to contact us.

PERSONAL ALLOWANCES AND RELIEFS

Minimising your personal tax bill.

ISAs

Maximising your tax-free savings.

PENSIONS

Saving for your retirement

INHERITANCE TAX

Reducing your estate’s tax burden.

PROPERTY TAXES

Understanding your obligations

CAPITAL GAINS TAX

Rules, exemptions, and planning opportunities.

BUSINESS ASSET DISPOSAL RELIEF

Reducing capital gains tax when selling your business.

NON-DOMICILED TAX

Understanding your residency and domicile status.

TAX-EFFICIENT STAFF BENEFITS

Maximising employee rewards while saving on tax

CORPORATION TAX

Understanding rates and planning opportunities.

VAT

Simplifying compliance and saving on VAT.

PENALTIES

The cost of non-compliance.

Minimising your personal tax bill

For the 2025/26 tax year, the standard Personal Allowance remains at £12,570, meaning you can earn up to this amount before paying Income Tax. Earnings above this threshold are taxed at rates of 20% (basic rate), 40% (higher rate), and 45% (additional rate) in England, Wales, and Northern Ireland. In Scotland, different tax bands apply.

If your income exceeds £100,000, your Personal Allowance decreases by £1 for every £2 earned over this limit. This effectively creates a 60% marginal tax rate on income between £100,000 and £125,140, as the entire Personal Allowance is withdrawn within this band.

Marriage allowance

If you’re married or in a civil partnership, and one partner has an income below the Personal Allowance while the other is a basic-rate taxpayer, you may benefit from the Marriage Allowance. This allows the lower-earning partner to transfer £1,260 of their unused Personal Allowance to their partner, potentially reducing the tax bill by up to £252.

Tax on savings and investments

- Personal savings allowance: Basic-rate taxpayers can earn up to £1,000 in savings interest tax-free, while higher-rate taxpayers have an allowance of £500. Additional-rate taxpayers do not receive this allowance.

- Dividend allowance: For the 2025/26 tax year, the Dividend Allowance remains at £500. Dividend income exceeding this amount is taxed at 8.75% (basic rate), 33.75% (higher rate), or 39.35% (additional rate).

Key considerations

- Utilising allowances: Ensure both you and your spouse or civil partner fully utilise your Personal Allowances. Transferring income-generating assets between partners can help achieve this.

- Reducing high marginal tax rates: To retain your total Personal Allowance and avoid the 60% marginal tax rate, consider making pension contributions or charitable donations to reduce your adjusted net income below £100,000.

- Tax-efficient alternatives: To minimise tax liabilities, explore tax-efficient alternatives to bonuses or salary increases, such as employer pension contributions or salary sacrifice arrangements.

- Investments: The Enterprise Investment Scheme (EIS) and Seed Enterprise Investment Scheme (SEIS) offer generous income tax reliefs (30% for EIS and 50% for SEIS) while encouraging investment in early-stage companies. They can be particularly effective in reducing personal tax liabilities and are worth considering as part of a broader tax strategy.

- Rent-a-Room relief: If you rent out a furnished room in your home, you can earn up to £7,500 tax-free under the Rent-a-Room scheme.

By proactively managing your personal allowances and reliefs, you can effectively minimise your tax bill and optimise your financial position for the 2025/26 tax year.

Maximising your tax-free savings

Individual Savings Accounts (ISAs) offer a tax-efficient way to save or invest, with various types catering to different financial goals. For the 2025/26 tax year, the overall ISA allowance remains at £20,000.

Types of ISAs and their limits

- Cash ISA: Allows you to save cash without paying tax on the interest earned. You can allocate up to a £20,000 allowance to a Cash ISA.

- Stocks and Shares ISA: Enables investments in stocks, shares, and funds with tax-free growth and dividends. You can invest up to £20,000 or split the allowance between different ISAs.

- Innovative Finance ISA: Includes peer-to-peer loans and crowdfunding investments. The maximum investment is up to £20,000, subject to the overall ISA limit.

- Lifetime ISA (LISA): Designed for individuals aged 18 to 39 to save for a first home or retirement. You can contribute up to £4,000 per year, with the government adding a 25% bonus (up to £1,000 annually). Contributions to a LISA count towards the overall £20,000 ISA allowance.

Junior ISA

For individuals under 18, a Junior ISA allows savings of up to £9,000 per tax year, with tax-free interest or investment growth.

Key considerations

● Use it or lose it: The ISA allowance does not roll over; ensure you utilise your allowance within the tax year to maximise tax-free savings.

● Strategic allocation: Depending on your financial goals, consider how to allocate funds across different ISAs to optimise tax benefits.

● Spousal contributions: If you have maximised your ISA allowance, assess whether your spouse or civil partner has unused allowance to enhance tax-free savings further.

● First-time buyers: Utilising a LISA can be advantageous for first-time home purchases, as it provides a government bonus to boost savings.

By effectively leveraging ISAs, you can enhance your tax-free savings and investments, aligning with your financial objectives for the 2025/26 tax year.

Saving for your retirement

Maximising your pension contributions before the end of the tax year is one of the most effective ways to reduce your taxable income and save for retirement. Pension contributions benefit from tax relief, which can make them particularly attractive for higher earners.

For the 2025/26 tax year, the annual pension allowance remains at £60,000. This includes all contributions you, your employer, and any third parties make. However, this allowance may be tapered for individuals with threshold income over £200,000 and an adjusted annual income of over £260,000, reducing by £1 for every £2 above this threshold. The minimum annual allowance for high earners is £10,000, which applies to those with a total income of £360,000 or more.

Suppose you had a pension scheme during a previous tax year but didn’t fully use your allowance. In that case, you can carry forward unused amounts for up to three years, provided you meet the eligibility criteria.

Key considerations

- Carry forward unused allowances: Review any unused allowances from 2022/23, 2023/24, or 2024/25 tax years to see if you can contribute more this year.

- Tax relief for higher earners: Ensure you claim any additional tax relief on pension contributions. Higher-rate taxpayers can claim an extra 20% tax relief, and additional-rate taxpayers can claim 25%, often via self-assessment.

- Inheritance tax benefits: Pension funds are typically excluded from your estate for inheritance tax purposes. Maximising contributions can help with long-term estate planning.

- Over-55s considerations: If you’re over 55 and considering accessing your pension, ensure you understand the potential tax implications, such as triggering the money purchase annual allowance (MPAA), which limits future contributions to £10,000.

Important deadlines

Ensure all contributions are paid into your pension scheme by 5 April 2025 to qualify for tax relief in the 2024/25 tax year. Employer contributions must be paid before the company’s financial year-end to receive corporation tax relief in the same accounting period.

By taking advantage of pension contribution rules and tax reliefs, you can optimise your retirement savings while reducing your tax liability for the current tax year.

Reducing your estate’s tax burden

Inheritance tax (IHT) is charged at 40% on the value of your estate that exceeds the nil-rate band, which remains at £325,000 for the 2025/26 tax year. An additional residence nil-rate band (RNRB) of £175,000 is available if your home (or a share of it) is left to direct descendants. When combined, this means a total IHT-free threshold of up to £500,000 for individuals or £1 million for married couples or civil partners.

For estates worth over £2 million, the RNRB tapers by £1 for every £2 above this threshold. It’s important to note that unused allowances can be transferred to a surviving spouse or civil partner, doubling the threshold available on the second death.

Gifts made during your lifetime are generally exempt from IHT if you survive for seven years after making them. However, gifts within this timeframe may still be subject to tax. Taper relief could reduce the tax rate on gifts made between three and seven years before death.

Key considerations

- Make use of exemptions: The annual gift exemption allows you to give up to £3,000 tax-free each year. You can also make small gifts of up to £250 per person, wedding gifts, or gifts from surplus income without triggering IHT.

- Plan lifetime giving: Consider using the seven-year rule for larger gifts to reduce the value of your estate over time.

- Trusts and estate planning: Putting assets into a trust can help reduce the value of your estate subject to IHT, but it’s important to get professional advice to ensure compliance.

- Residence nil-rate band: Review your will to ensure your estate qualifies for the RNRB if applicable, and confirm how property is passed to direct descendants.

- Spousal exemptions: Ensure you take advantage of the full spousal transfer of unused IHT allowances to maximise the tax-free thresholds on the second death.

- Business and agricultural reliefs: For qualifying assets, investigate reliefs that could reduce IHT on business or agricultural property.

By planning your estate effectively, you can reduce the amount of IHT payable and ensure your assets are passed on to your loved ones in the most tax-efficient way possible. If you’re unsure about the best strategy for your situation, we’re here to help.

Understanding your obligations

Property taxes apply to various transactions and ownership scenarios, from buying a new home to managing additional properties. With different rules across the UK, understanding your obligations is key to effective tax planning.

Stamp duty land tax (SDLT) – England and Northern Ireland

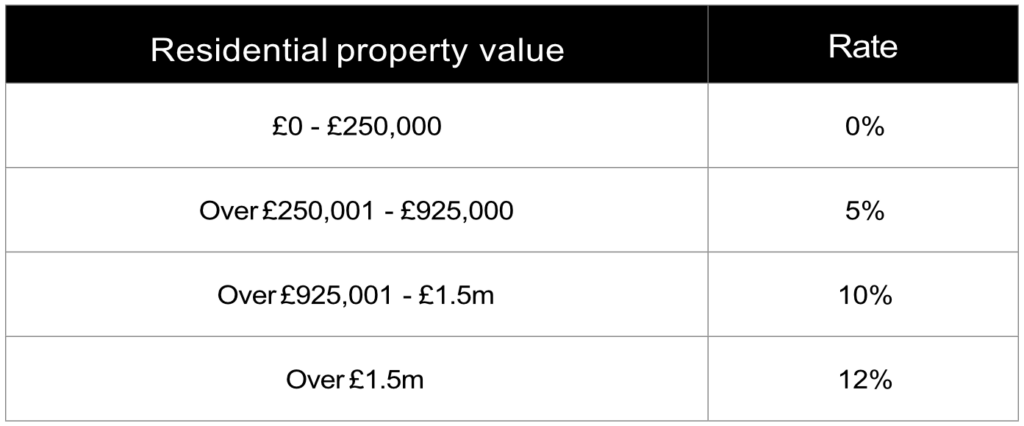

In England and Northern Ireland, stamp duty land tax is payable on property purchases above £250,000 until 31 March 2025. For first-time buyers, the nil-rate threshold is higher at £425,000 for properties valued up to £625,000.

A 3% surcharge applies to additional residential properties on top of the standard SDLT rates.

Upcoming changes (effective from 1 April 2025):

- Standard residential purchases: The nil-rate threshold will decrease to £125,000. This means SDLT will be payable on properties valued above £125,000.

- First-time buyers: The nil-rate threshold for first-time buyers will reduce to £300,000 for properties valued up to £500,000. For properties worth between £300,001 and £500,000, a 5% SDLT rate will apply to the portion above £300,000. Properties over £500,000 will not be eligible for first-time buyer relief, and standard rates will apply.

Land and buildings transaction tax (LBTT) – Scotland

In Scotland, LBTT applies to residential property purchases above £145,000. First-time buyers pay no tax on properties worth up to £175,000. Rates include:

- £0-£145,000: 0%

- £145,001-£250,000: 2%

- £250,001-£325,000: 5%

- £325,001-£750,000: 10%

- Over £750,000: 12%

An 8% additional dwelling supplement applies to purchases of second homes or buy-to-let properties worth over £40,000.

Land transaction tax (LTT) – Wales

In Wales, LTT applies to residential property purchases above £225,000 for those who don’t own other properties. The rates are:

- £0-£225,000: 0%

- £225,001-£400,000: 6%

- £400,001-£750,000: 7.5%

- £750,001-£1.5 million: 10%

- Over £1.5 million: 12%

A higher rate of residential property tax applies to additional residential properties purchased in Wales.

Key considerations

- First-time buyer reliefs: Ensure you meet the criteria to benefit from higher nil-rate bands for first-time buyers.

- Additional property planning: Factor in the surcharge when purchasing buy-to-let properties or second homes.

- Deferred or gifted property: Consider the tax implications of transferring or gifting property, which may attract capital gains tax or inheritance tax.

- Regional differences: Property tax rates and thresholds vary significantly across the UK, so check the rules specific to your location.

- Timing of purchases: If you plan to buy a property, consider how upcoming tax changes (e.g. the end of temporary SDLT relief) might impact your liabilities.

Property taxes can significantly impact your overall financial position, so careful planning is essential. If you need help navigating these taxes or optimising your property transactions, contact us.

Rules, exemptions, and planning opportunities

Capital gains tax (CGT) is payable on the profit you make when selling or disposing of certain assets, such as property, shares, or business assets, that have increased in value. The tax applies to the gain, not the total amount received. With the annual CGT exemption significantly reduced for the 2024/25 and 2025/26 tax years, careful planning is more important than ever.

Key allowances for 2025/26

- The annual CGT exemption is £3,000. Gains above this threshold are subject to tax.

- Married couples and civil partners can each claim the £3,000 exemption, allowing a combined total of £6,000.

- Gains on most assets are taxed at 18% (basic-rate taxpayers) or 24% (higher- and additional-rate taxpayers).

- Trustees typically pay 24% on gains from both residential property and other chargeable assets.

Key considerations

- Use your annual exemption: Ensure you make the most of the £3,000 exemption before 5 April 2025, as unused allowances cannot be carried forward.

- Spousal and partner planning: Transferring assets to a spouse or civil partner before disposal can allow both exemptions to be used, reducing CGT liability.

- Offsetting losses: If you have assets that have fallen in value, consider selling them to realise a loss, which can be offset against your gains in the same tax year or carried forward.

- Deferring or rolling over gains: Certain investments, such as those qualifying for the Enterprise Investment Scheme (EIS) or Seed Enterprise Investment Scheme (SEIS), may allow gains to be deferred or rolled over into new investments.

- Business reliefs: If you’re selling a business, investigate whether you qualify for business asset disposal relief (formerly entrepreneurs’ relief), which reduces CGT on qualifying gains to 10%. However, this rate is set to increase to 14% for disposals made on or after 6 April 2025, and further to 18% for disposals on or after 6 April 2026.

- Main residence exemption: If you sell your main home, you may qualify for private residence relief, which exempts most or all of the gain from CGT. Consider making a main residence election for second homes or rental properties to optimise relief.

Important deadlines

If you sell a residential property that is not your main residence, you must report the gain and pay any CGT owed within 60 days of the sale completion. For other assets, CGT is usually paid via self-assessment by 31 January following the tax year of the disposal.

By understanding and planning for CGT, you can minimise your tax liability and make the most of the available reliefs and exemptions. We’re here to guide you if you need help with a specific disposal or understanding your obligations.

Reducing capital gains tax when selling your business

Business asset disposal relief (formerly known as entrepreneurs’ relief) allows qualifying business owners to reduce the rate of capital gains tax (CGT) on the disposal of their business or business assets. Instead of the standard CGT rates, gains that qualify for this relief are taxed at a reduced rate of 10%, up to a lifetime limit of £1 million. From 6 April 2025, the tax rate on gains qualifying for BADR will increase from 10% to 14%.

Eligibility criteria

To qualify for business asset disposal relief, the following conditions must be met:

Ownership: You must have owned the business or business assets for at least two years prior to the sale.

Type of business: The business must be a trading business, not an investment business.

Shares and securities: If selling shares or securities, the company must be a trading company, and you must hold at least 5% of both:

The shares and voting rights, and

Either the profits available for distribution or disposal proceeds if the company is sold.

Enterprise management incentive (EMI) shares: Special rules apply, with some conditions relaxed, for shares acquired through an EMI scheme.

Lifetime limit

A lifetime limit of £1 million applies to the total gains eligible for business asset disposal relief. If you have already claimed relief on gains reaching this amount, any further disposals will not qualify for the reduced CGT rate.

Key considerations

- Plan ahead: Ensure you meet the two-year ownership and employment criteria before disposing of your business or assets.

- Review shareholdings: If you hold shares in a trading company, confirm that your ownership and voting rights meet the 5% threshold.

- Closing your business: If you’re closing your business, remember that business assets must be disposed of within three years to qualify for relief.

- Lifetime limit tracking: If you’ve claimed business asset disposal relief in the past, check your remaining lifetime limit to assess eligibility.

- Partnerships and sole traders: Relief may apply to assets disposed of as part of your business, such as land or property used by the business, provided other conditions are met.

Additional notes

While this relief provides a valuable tax-saving opportunity, ensuring compliance with the qualifying conditions is essential. Complex scenarios, such as partial disposals or restructuring, may require additional guidance.

By taking advantage of business asset disposal relief, you can significantly reduce the tax liability on the sale of your business or qualifying assets. If you need assistance in planning your disposal or ensuring eligibility, we’re here to help.

Understanding your residency and domicile status

The UK government has announced significant reforms to the taxation of non-UK domiciled individuals, commonly known as ‘non-doms’. These changes, effective from 6 April 2025, aim to modernise and simplify the tax system, making it fairer and more competitive.

Key changes:

- Abolition of the non-dom regime: The existing non-dom tax regime will be replaced with a residence-based system. This means that tax liability will be determined by an individual’s tax residence status rather than their domicile.

- Four-year foreign income and gains exemption: New arrivals to the UK, who have not been tax residents in the previous 10 years, will benefit from a four-year exemption on foreign income and gains. During this period, they will not be subject to UK tax on these overseas earnings.

- Inheritance tax (IHT) changes: The concept of domicile will no longer be relevant for IHT purposes. Instead, a residence-based system will be implemented, potentially altering the scope of IHT liabilities for individuals with international ties.

Implications:

- Existing non-doms: Individuals currently benefiting from the non-dom regime will need to reassess their tax positions in light of these changes. The shift to a residence-based system may result in increased tax liabilities on worldwide income and gains.

- New arrivals: The four-year exemption provides a transitional period for new UK residents to adjust their financial affairs. However, they will be subject to UK tax on global income and gains after this period.

- Estate planning: Moving to a residence-based IHT system necessitates reviewing estate planning strategies, especially for those with assets in multiple jurisdictions.

Action points:

- Review tax status: Individuals affected by these changes should consult with tax advisers to understand the full impact on their financial situation.

- Plan ahead: With the abolition of the non-dom regime set for April 2025, there is a window to implement tax-efficient strategies before the new rules take effect.

- Stay informed: As the government releases further details and guidance, staying updated will be crucial to ensure compliance and optimise tax planning.

These reforms represent a significant shift in the UK’s approach to taxing non-domiciled individuals. Proactive planning and professional advice are essential to navigate this evolving landscape effectively.

Maximising employee rewards while saving on tax

Offering tax-efficient staff benefits is a great way for employers to reward employees without incurring significant tax or National Insurance costs. These benefits can help reduce overall tax liabilities for employers and employees while enhancing workplace satisfaction.

Working-from-home allowance

If employees are required to work from home, they may be able to claim tax relief of £6 per week or £26 per month from HMRC. Alternatively, employers can pay this allowance to employees tax-free via payroll.

Key points:

- The allowance only applies if employees are required to work from home, not if they choose to.

- Hybrid working policies where homeworking is optional may not qualify.

Mobile phones

Employers can provide each employee with one mobile phone, including its line rental and the cost of private calls, without it being considered a taxable benefit-in-kind. This exemption applies only if the employer retains ownership of the phone and the contract is between the employer and the service provider. If the contract is in the employee’s name and the employer reimburses the costs, the payments are treated as taxable earnings subject to PAYE tax and national insurance contributions.

Electric vehicles

Providing company cars with low emissions, such as electric or plug-in hybrid vehicles, offers significant tax advantages.

- Employees pay a 3% benefit-in-kind tax on fully electric cars for 2025/26. This rate is scheduled to increase by 1% each subsequent tax year, reaching 4% in 2026/27 and 5% in 2027/28.

- Hybrid cars with CO₂ emissions of no more than 50g/km and an electric range of over 130 miles or above also qualify for the 3% rate.

- Employers can save on Class 1A National Insurance and may claim capital allowances on electric vehicles.

Employers can also offer charging facilities at work as a tax-free benefit.

Salary sacrifice schemes

Salary sacrifice arrangements allow employees to exchange part of their salary for benefits, such as:

- Pension contributions

- Electric vehicles

- Childcare vouchers (if still eligible)

- Cycle-to-work schemes

These schemes can reduce taxable income and save on income tax and national insurance.

Trivial benefits

Employers can provide small, non-cash benefits worth up to £50 per employee tax-free. To qualify, the benefit:

- Must not be cash or a voucher that can be converted into cash.

- Cannot be linked to performance or contractual obligations.

The exemption for directors of close companies is limited to six qualifying benefits per tax year, with a total annual value of £300.

Key considerations

- Benefit options: Review the range of benefits offered to ensure they are tax-efficient and attractive to employees.

- Salary sacrifice impacts: Ensure employees understand the potential effect of salary sacrifice arrangements on their pension contributions and statutory benefits, such as maternity pay.

- Employee engagement: Promote awareness of available benefits to maximise uptake and employee satisfaction.

- Compliance: Keep detailed records of benefits provided to ensure compliance with HMRC rules.

By leveraging tax-efficient staff benefits, employers can reduce their overall tax liabilities while providing meaningful rewards to their teams. Get in touch for tailored advice on implementing these schemes in your business.

Understanding rates and planning opportunities

Corporation tax is a key consideration for businesses operating in the UK. Understanding the applicable rates, reliefs, and deadlines for the 2025/26 financial year is essential for effective tax planning.

Corporation tax rates

The corporation tax rate structure is as follows:

- Main rate (25%): Applies to companies with profits over £250,000.

- Small profits rate (19%): Applies to companies earning £50,000 or less.

- Marginal relief: For companies with profits between £50,001 and £250,000, marginal relief reduces the effective tax rate below 25%. The relief tapers as profits approach the £250,000 threshold.

The profit thresholds are proportionately reduced if your company has associated companies or a shorter accounting period.

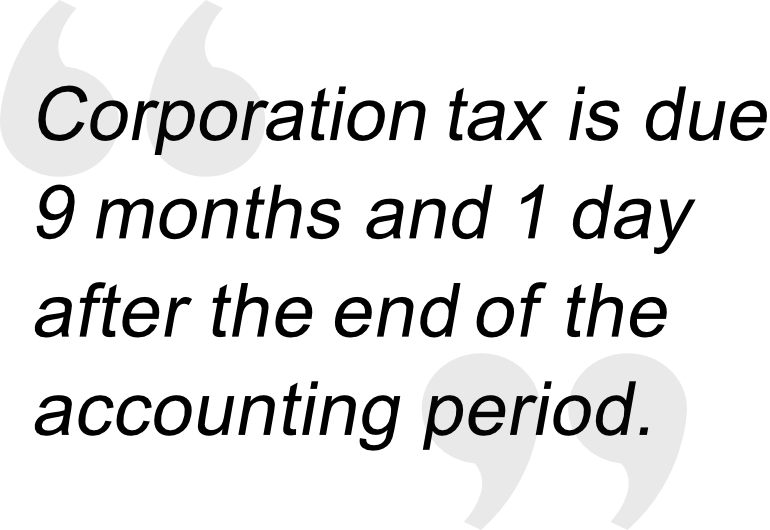

Payment deadlines

- Small companies: Corporation tax is due 9 months and 1 day after the end of the accounting period.

- Large companies: Companies with annual profits exceeding £1.5 million must pay corporation tax in quarterly instalments.

- Very large companies: Companies with annual profits over £20 million have earlier instalment deadlines.

Key deductions and reliefs

- Business expenses:

Only expenses incurred “wholly and exclusively” for business purposes are deductible.

Examples include salaries, rent, utilities, marketing, and professional fees. - Capital allowances:

Over time, deduct the cost of qualifying capital assets, such as equipment, machinery, or vehicles.

The annual investment allowance (AIA) allows a 100% deduction on qualifying expenditures up to £1 million. - Research and development (R&D) tax credits:

For accounting periods starting between 1 April 2023 and 31 March 2024, small and medium-sized enterprises (SMEs) can claim a 186% deduction on qualifying R&D costs.

Large companies may claim the R&D expenditure credit (RDEC), worth 20% of qualifying expenditure.

For periods starting on or after 1 April 2024, a new merged R&D tax relief scheme applies. Under this scheme, all companies can claim a taxable R&D expenditure credit at a rate of 20% on qualifying costs. R&D-intensive SMEs may also benefit from enhanced R&D intensive support, which allows for a 186% deduction and a payable tax credit of up to 14.5% of surrenderable losses.

4. Patent box relief:

Profits from patented inventions and certain intellectual property can benefit from a reduced corporation tax rate of 10%.

5. Loss relief:

Trading losses can be carried forward to offset future profits or carried back to offset the previous year’s taxable profits.

Key considerations

- Tax-efficient profit extraction: Plan how to withdraw profits, balancing dividends, salary, and benefits to optimise tax efficiency.

- Director’s bonuses: If you plan to pay bonuses, ensure they are accrued in your annual accounts and paid within nine months of the year-end to claim a deduction in the current accounting period.

- Pension contributions: Employer contributions to pensions are deductible but must be paid before the year-end to qualify for relief.

- Associated companies: Monitor the impact of associated companies on your profit thresholds for marginal relief or instalment payments.

- Investment decisions: Make the most of the AIA or other capital allowances to reduce taxable profits.

Corporation tax planning is an essential part of running a business. Understanding the rates, reliefs, and deductions available can minimise your tax liabilities and improve your cashflow. For personalised advice on managing your corporation tax obligations, contact us.

Simplifying compliance and saving on VAT

Value Added Tax (VAT) is a consumption tax charged on the sale of goods and services. Compliance is essential for businesses registered for VAT, and proper planning can help minimise costs and improve cashflow.

VAT registration thresholds

For the 2025/26 tax year:

- Registration threshold: Businesses must register for VAT if their taxable turnover exceeds £90,000 in any 12-month period or is expected to exceed this amount in the next 30 days alone.

- Deregistration threshold: Businesses can voluntarily deregister if their turnover falls below £88,000 over 12 months.

Voluntary registration is an option for businesses below the threshold, particularly if they have significant input VAT to reclaim.

VAT rates

- Standard rate: 20% (applies to most goods and services).

- Reduced rate: 5% (applies to certain goods and services, such as energy-saving materials).

- Zero rate: 0% (applies to specific items like most cold food, children’s clothing, and books).

Some goods and services are exempt or outside the scope of VAT, but these do not allow input VAT recovery.

Making Tax Digital (MTD) for VAT

Regardless of turnover, all VAT-registered businesses must comply with Making Tax Digital (MTD) rules. This includes:

- Keeping digital VAT records.

- Submitting VAT returns via MTD-compatible software.

From January 2023, HMRC implemented stricter penalties for late submissions under a points-based system.

VAT schemes

Simplify VAT accounting and potentially save money using these schemes:

- Flat Rate Scheme: Designed for businesses with a VAT-exclusive turnover of £150,000 or less. Participants pay a fixed percentage of their turnover as VAT, which can simplify record-keeping. However, once turnover exceeds £230,000 (including VAT), businesses must exit the scheme.

- Cash Accounting Scheme: Suitable for businesses with a VAT-exclusive turnover up to £1.35 million. Under this scheme, VAT is accounted for only when payment is actually made or received, aiding in cashflow management. Exiting the scheme is required if turnover surpasses £1.6 million (VAT exclusive).

- Annual Accounting Scheme: Allows businesses with a VAT-exclusive turnover of £1.35 million or less to file a single annual VAT return instead of quarterly ones, accompanied by advance instalment payments. Departure from the scheme is necessary if turnover exceeds £1.6 million (VAT exclusive).

Each scheme offers distinct advantages and considerations. Consulting with a tax professional can help determine the most suitable option for your business.

Key considerations

- Reclaiming VAT:

Ensure you are reclaiming VAT only on allowable expenses. For example, VAT on cars is generally only reclaimable if the vehicle is used exclusively for business purposes.

Check eligibility for VAT bad debt relief if customers fail to pay within six months. - Private use adjustments:

Adjust input VAT claims to reflect the business portion only for assets used partly for personal use. - Pre-registration expenses:

If you are newly registered, you can reclaim VAT on goods purchased in the four years prior to registration, provided they are still used in the business, and services purchased in the six months prior to registration.

4. VAT on property:

VAT rules for property transactions can be complex. Seek advice for decisions involving commercial or residential property, as they may attract VAT or require an option to tax.

5. Export and import rules:

Ensure compliance with post-Brexit VAT rules for international trade, including applying the correct rates and procedures for exports and imports.

By understanding VAT rules and schemes, businesses can remain compliant while maximising opportunities to save costs. If you need assistance with VAT registration, filing, or planning, we’re here to help.

The cost of non-compliance

Tax compliance is crucial to avoid penalties and interest from HMRC. Whether it’s filing late returns, making incorrect submissions, or failing to register for a tax obligation, non-compliance can result in significant financial and reputational costs.

Income tax self-assessment penalties

Missing the self-assessment tax return deadline of 31 January 2025 incurs penalties:

- 1 day late: £100 fixed penalty, regardless of whether tax is owed.

- 3 months late: £10 per day for up to 90 days (maximum £900).

- 6 months late: The greater of either 5% of the tax due or £300.

- 12 months late: The greater of 5% of the tax due or £300. In cases of deliberate withholding of information or failure to notify HMRC, penalties can reach up to 100% of the tax owed.

Late payment penalties:

- 30 days late: 5% of the unpaid tax.

- 6 months late: An additional 5%.

- 12 months late: Another 5%.

Interest on late payments is charged at the Bank of England base rate plus 2.5%, currently 7.25%, but subject to change.

Corporation tax penalties

Corporation tax returns must be filed within 12 months of the end of the accounting period. However, any tax due must be paid earlier – within 9 months and 1 day of the end of the accounting period. Late submissions result in:

- £100 for being up to 3 months late.

- An additional £100 for being between 3 and 6 months late.

- Additional penalties based on the tax due for returns over 6 months late.

Late payment penalties depend on the length of delay and may include surcharges or interest. If the return is submitted late three years in a row, the penalties increase from £100 to £500.

VAT penalties

HMRC has implemented a system for late VAT payments, effective from 1 January 2023. This system introduces two types of penalties: the first and second late payment penalties.

First late payment penalty:

- Timing: Applies if the VAT payment is 16 or more days overdue.

- Calculation: 2% of the VAT owed on day 15. An additional 2% of the VAT owed on day 30 if the payment remains outstanding.

Second late payment penalty:

- Timing: Applies if the VAT payment is 31 or more days overdue.

- Calculation: A daily penalty charged at 4% per annum on the outstanding balance, accruing from day 31 until the debt is paid in full.

HMRC charges interest on any unpaid VAT from the first day the payment is overdue until it is paid in full. The interest rate is set at the Bank of England base rate plus 2.5%.

For more detailed information, refer to HMRC’s official guidance on late payment penalties.

Inheritance tax penalties

Failure to submit an accurate inheritance tax return by the due date can result in:

- Up to 6 months late: A fixed £100 penalty, regardless of the tax owed.

- 6 to 12 months late: An additional £100 penalty may apply.

- Over 12 months late: A penalty of up to £3,000 can be charged.

Interest on unpaid tax is also charged at the Bank of England base rate plus 2.5%, similar to VAT.

Key considerations

- Meet deadlines: Ensure all tax returns and payments are made on time to avoid penalties and interest.

- Check accuracy: Submitting incorrect returns, even unintentionally, can result in penalties. Double-check figures or seek professional advice if in doubt.

- Proactive communication: If you can’t pay on time, contact HMRC to agree on a payment plan before the due date to reduce penalty exposure.

- Stay organised: Keep accurate records and ensure you know all tax obligations relevant to your circumstances.

- Monitor updates: Penalty rates and interest are subject to change, so stay informed of the latest HMRC rules.

You can avoid unnecessary penalties and ensure smooth tax operations by staying compliant with filing deadlines and payment obligations. If you’re concerned about potential liabilities or need assistance managing your tax affairs, we’re here to support you.

Important information

How tax charges (or tax relief, as appropriate) are applied depends on individual circumstances and may be subject to future change. ISA and pension eligibility depend on individual circumstances.

FCA regulation applies to certain regulated activities, products, and services, but it does not necessarily apply to all tax-planning activities and services.

This document is solely for information purposes and nothing in it is intended to constitute advice or a recommendation.

While considerable care has been taken to ensure the information in this document is accurate and up-to-date, no warranty is given as to its accuracy or completeness.

Contact Us for tax planning advice.